Thích

Thích

Keppel Land's new retail mall in Ho Chi Minh City's Saigon Centre is part of plans to increase its presence in Vietnam anchored by Japanese retail giant Takashimaya.

Future supply to grow by 25%, mostly in the East

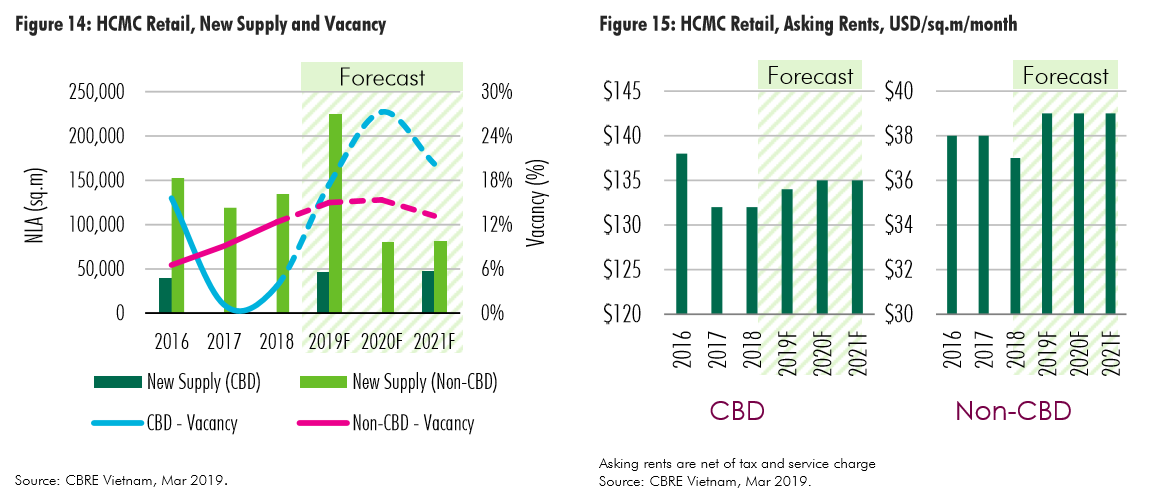

HCMC’s current retail supply reached almost one million sq. m NLA. 80% of total stock are shopping centres, 14% are retail podiums and department stores make up the remaining share. In 2018, HCMC welcomed three new large-scale shopping centers each of which measured 25,000 to 60,000 sq. m NLA. Compared to 2017, when eight out of ten new projects in HCMC were retail podiums with small scale, the new supply of 2018 has now provided more quality spaces.

Pipeline of seven new shopping centres, with sizes ranging from 20,000 sq. m NLA to 60,000 sq. m NLA per project and totaling more than 247,000 sq.m NLA, are expected to enter the market in 2019. Except Union Square (which will be relaunched following renovation), six other projects are all located in non-CBD areas.

More than 51% of total new stock is developed in the East, while only 9.2% of that is in the city center. No future supply will be posted for the West.

These upcoming projects are progressing relatively slow compared to their initial planning. In the coming years, as further large-scale condominium projects would be completed, a significant supply of retail podiums is expected to surge accordingly.

In terms of format, shopping centers are expected to continue being the dominant retail format. The closure of some Parkson department stores in HCMC has proved that stand-alone department stores have failed to deliver adequate shopping experiences for customers and to adapt to rapid changes in consumer behaviors.

In terms of shop format, the trend of pop-up retail will continue in the future, especially within the high-end and mid-end segments. These stores have special, unique and interesting designs that trigger curiosity in customers, luring them to visit the store. HCMC has been chosen by many foreign and local brands to open their first store in Vietnam. In order to test an immature market such as HCMC, a pop-up shop is a low-risk starting point. An increasing number of local brands have also adopted this pop-up model as a great way to test an area and potential clientele. Retailers have correspondingly taken advantage of the peak shopping season by hosting holiday pop-up shops at short-term retail spots in busy shopping centres such as Saigon Centre.

Rents to rise by 5% on average in 2019

In 2018, the significant disparity in supply between CBD and non-CBD areas has led to a great divergence of rents with asking rents for an area of 80–250 sq. m. on ground floor and first floor in CBD area ranging from US$75/sq. m/month to US$156/sq. m/month. Moreover, new retailers aiming at CBD area face lower hand in negotiating with landlords and developers. In 2018, vacancy rates in the CBD area were extremely low due to limited supply in this area. The vacancy rates in non-CBD areas decreased owing to good absorption of new supply.

In 2019, increasing new supply in both CBD and non-CBD areas is expected to raise vacancy rates in these areas, to 17.5% and 15.3%, respectively. Despite scarce supply in CBD areas, occupancy rate of the new supply in 2019 (to open after renovation) will not be extreme given its large scale and high rental rate, leading to higher vacancy rates in CBD areas.

In 2019, new supply in prime locations of both CBD and non-CBD areas, typically offering higher asking rents, are expected to push average rents in these areas to US$134/sq. m/month and US$39/sq. m/month, respectively. Afterwards, there will be two to three projects each year, and these projects are scattered in diverse locations of the city. Therefore, average rental rates are forecasted to remain stable for 2020 and 2021.

Moreover, retail podiums at residential projects still attract a decent flow of tenants, especially from F&B and activity-based segments. This is the result of flexibility in terms of rental agreements offered by private landlords. Tenants will keep looking at a revenue sharing model with the property owners when they open a new outlet. This model, which has become more popular in the city, helps retailers to reduce rental costs, at least in the initial months of opening an outlet, when the business is not yet profitable and when footfall is lower.

New entrants to the market

Among brands coming to Ho Chi Minh in 2018, more than half are from the Asia-Pacific region, most of which are from Asia including Taiwan and Japan. Most new entrants were from F&B and mid-range fashion segments. Beverage retailers such as milk tea brands from Taiwan were particularly active in the market last year, through either opening their footprint or expanding their footprint in the city. Several shopping malls have increased their F&B presence to more than 20% including the three latest projects, Estella Place, Vincom Center Landmark 81 and Van Hanh Mall. There will be a further shift away from traditional shopping mall’s tenant mixes towards an increased focus on entertainment and F&B. In 2019, F&B retailers from Asia Pacific nations, for example Hai Di Lao Hot Pot and Hachiban Ramen, together with specialist clothing brands from Europe namely FitFlop Footwear and Olivia Burtons, will enter HCMC market. Since CBD supply is scarce, tenants have little advantage in opting for locations while landlords have the opportunity to select their tenants.

Positive rental growth outlook

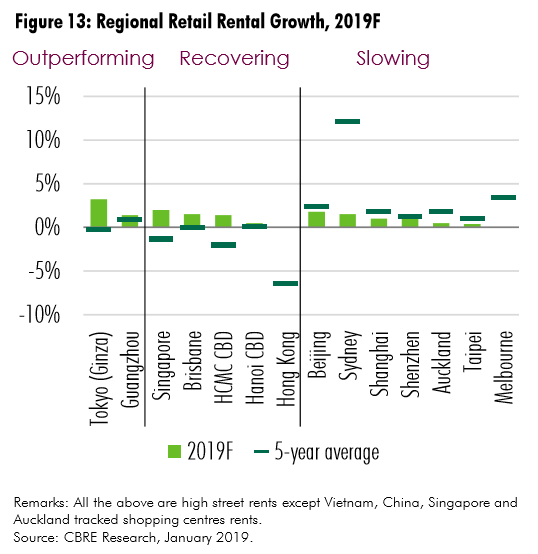

In 2019, retailers across Asia Pacific are expected to remain cautious after getting back on their feet, and around half of the major markets are to see growth slower than the average of the last five years.

In that context, HCMC appears to be one of the few markets with a bright rental growth outlook, where rental levels in 2019 are expected to rise quicker than the levels observed past five years. This is driven by new quality space to be introduced, which has been long sought after by international retailers wishing to enter or expand in the city. However, rental growth prospects will not be similar at all malls and all locations; locations of limited footfall and malls with outdated designs and irrelevant positioning would continue to struggle, unless changes arrive timely enough.

In HCMC, CBD rental growth will increase from 2019 onwards owing to completion of new projects. Stronger economic growth, high consumer confidence and more favorable FDI policies have enticed overseas retailers, which is a push for new rental levels in CBD areas.