Thích

Thích

A phone spare part production line of Samsung Electronics Vietnam. (Photo: VNA)

CBRE said in a recent statement that it had recorded an increase in production moving from China to alternative locations in Southeast Asia, including Vietnam, last year. While this trend is not new to many as cost of production in China continues to rise which makes relocation seem like a financially viable choice to many manufacturers, there are some other major drivers that can be worth highlighted.

According to a November 2018 survey conducted by the UBS Evidence Lab, which collected responses from 200 manufacturing companies with a significant export business or supply to exporters from China, relative to the size of their economies, ASEAN economies, especially Vietnam, may be well-placed to benefit from the production shift given Vietnam’s key economic fundamentals.

Aside from its high gross domestic product (GDP) growth, foreign direct investment and well-controlled inflation, the country continues to invest heavily in infrastructure and help manufacturers gain better access to key export markets by participating in several bilateral and multilateral trade agreements.

These drivers are on top of Vietnam’s competitive land acquisition cost and labor cost (versus that in China and other neighboring countries) which have been underlying drivers for China plus One that several surveys that pointed out.

CBRE experts said that industrial parks in the country achieved good occupancy rate of between 70 - 90 percent, and infrastructure connectivity played a major role in the occupiers’ location decision.

Government heavy investment into major infrastructure projects

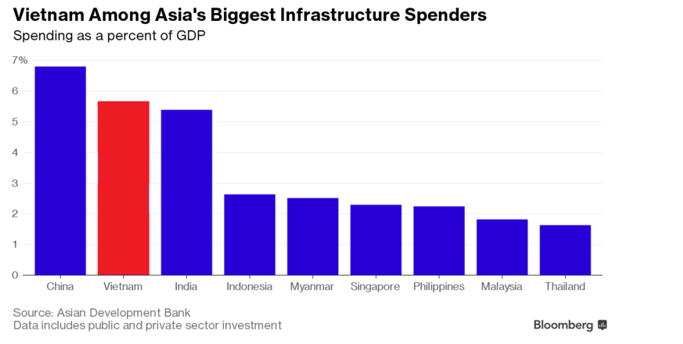

Vietnam government has spent billions of dollars to improve its infrastructure to help attract foreign investment. In fact, accordingly to statistics by Asian Development Bank & Bloomberg, Vietnam’s public and private sector infrastructure investment averaged 5.7% of GDP in recent years, the highest in Southeast Asia.

This direction has proven successful as improved major infrastructure projects such as new highways, expanded ports and airports, have enticed developers to follow with industrial parks being established or expanded in close distance to these infrastructures, and, in return, developers can offer this new infrastructure as part of their offering to attract occupiers from China (as highlighted in the above survey e.g. better infrastructure).

Vietnam active participation into bilateral and multilateral trade agreements & US – China trade war acts as a PUSHOVER

Vietnam have signed many agreements, including bilateral and multilateral agreements, with many nations. These include five free trade agreements within ASEAN, six more others with partners, including China, South Korea, Japan, India, Australia and New Zealand and four bilateral free trade agreements, including Vietnam – Japan FTA, Vietnam South Korea, CTPP and Vietnam – Europe FTA which expected to be signed in 2019.

Key benefits from these trade agreements is that they allow removal of duties among membership countries which help attract more manufacturers to set up production in Vietnam to retrieve tax benefit when they export to those markets.

Also, U.S. tariffs upon China coming on the ongoing trade war between these two countries is equivalent to a scenario of Vietnam essentially possessing a free trade agreement with the U.S. and Vietnam also poses a lower risk to trade war than China.

Under the assumption that all Chinese products would be subject to an additional 25% tariff, when Chinese products are hindered from export via that level of tax, effectively it is equivalent to a scenario of Vietnam essentially possessing a free trade agreement with the US.

It also means, in the short term, that Vietnam key exports like textile and garment, footwear, mobile phone, consumer electronics, wooden furniture, fisheries, bags, suitcases, and machinery could find better access into the US.

Workers produce earphones at a plant owned by electronics giant Samsung Vietnam. Vietnam enjoy considerable advantages in the production shift away from China. (Photo: VNA)

On reviewing the tariff list by product type, CBRE noted that TVs, mobile phones and several types of wearable technology have not been included on the current tariff list, so manufacturers in these sectors might seek to relocate part of their supply chain to Vietnam to mitigate the trade war risk and benefit from the country’s competitive costs.

- Apple production in Vietnam: The number of factories in Vietnam listed in Apple supplier list increased from 16 in 2015 to 22 in 2018. All of them are FDI companies. We noted that recently an Apple supplier (GoerTek) decided to move its AirPods production base (wireless earphones) to Vietnam.

- Samsung production in Vietnam: Samsung Electronics Co Ltd, the world’s biggest smartphone maker, said late last year it would cease operations at one of its mobile phone plants in China. (Source: Reuters). Localization rate jumped from 34% of total product value in 2014 to 57% in 2017. Currently 29 Vietnamese companies act as Samsung’s Tier-1 supplier (target: 2018: 35, 2019: 42, 2020: 50).

- LG Electronics Inc said it would stop producing smartphones in South Korea and move manufacturing to Hai Phong, Vietnam. The move will boost annual production capacity of its smartphone plant in Vietnam by 83 percent to 11 million handsets from the second half of 2019 (Source: Reuters).

In closing, looking at the remainder of 2019 and for the full 2020, CBRE sees an increase in industrial supply across Vietnam to benefit from this production shifting from China.

To well position themselves to cater to increasing demand, foreign developers would look for local partners with experience and big land bank to help fast track their market penetration as recently shown in a joint venture between Becamex and Warburg Pincus to form BW Industrial that can offer ready built & built to suit factories and warehouses in strategic locations in Vietnam e.g. 2 million sqm in 8 different sites in 5 key industrial cities including Bac Ninh (North Vietnam) and Binh Duong (South Vietnam).

As market and occupiers are getting more sophisticated, developers would need to provide a variety of products including, land lease, ready built factory & warehouse, built to suit facilities and Sale & Lease Back to bring more value to their clients.

For already-built factories in strategic locations, CBRE predicted that product specifications could evolve from traditional and conventional single storey to multistorey factories, with two to six floors. While high-rise stock in the market is still limited, this could become a new trend as Vietnam aims to attract advanced technology and light industries, which demand high-spec quality industrial spaces.

Senior Director and Head of the Research and Consulting Services for CBRE Vietnam Duong Thuy Dung said that as for the remainder of 2019 and the full 2020, there will be an increase in industrial property supply across Vietnam to benefit from this production shifting from China.